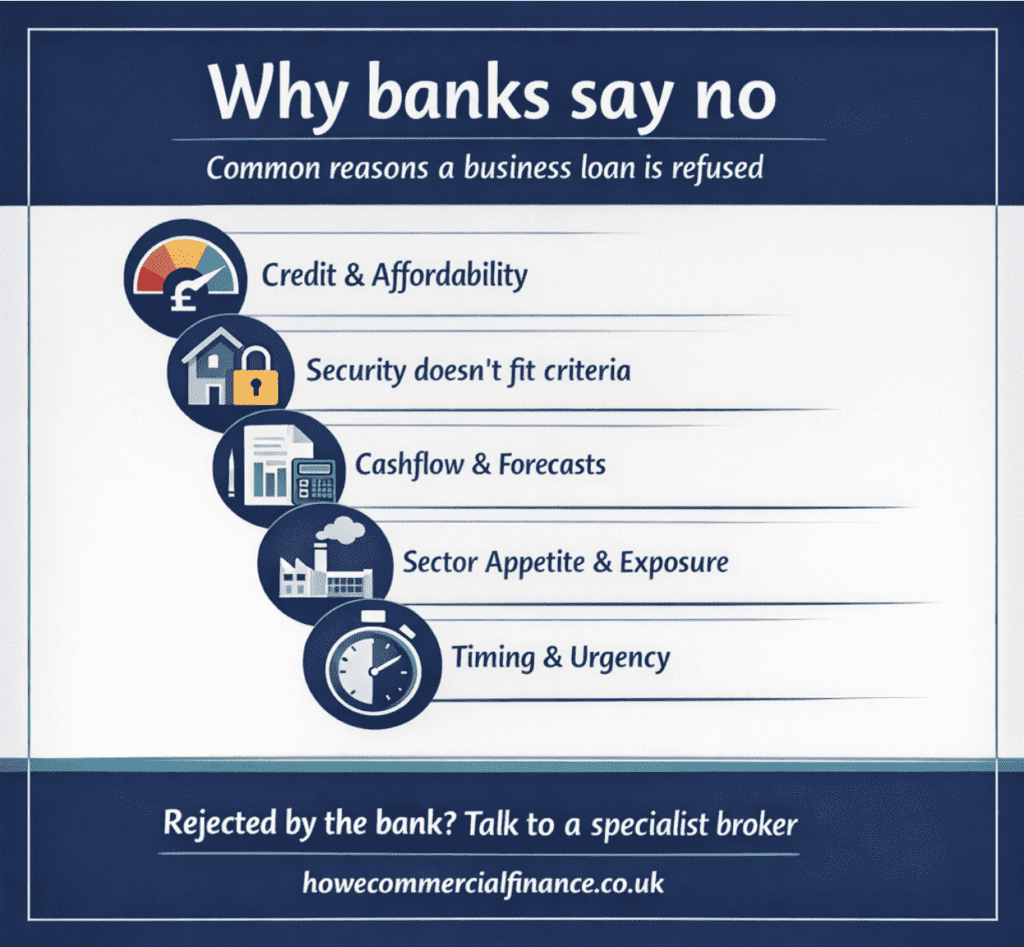

What banks often will not fund or will not fund quickly

1) Time-sensitive commercial property deals

Auctions. Tight completion deadlines. A chain wobble. A purchase you need to complete before the opportunity disappears.

Once a deposit is paid at auction, the clock starts. In most cases you have 20 working days to complete. Banks are not built for that. Their process simply cannot move at that pace.

This is exactly where bridging finance can be the right tool. Short-term funding that helps you complete, stabilise the position, and then refinance later when the timing is right.

One thing worth saying: having the right solicitor in place matters just as much as having the right finance. Speed on the lending side means nothing if the legal process becomes the bottleneck.

More on bridging finance: howecommercialfinance.co.uk/bridging-finance/

1b) Working capital for growing businesses

Banks also struggle with working capital for businesses that are growing but don’t yet have the paperwork to prove it.

Hospitality and retail are good examples. A business turning over more than £5,000 a month through its bank account can be genuinely viable, but if it’s relatively new and doesn’t have full financial accounts, the high street will often say no.

That’s not a reflection on the business. It’s a reflection on what the bank needs to feel comfortable. Specialist lenders assess these cases differently, looking at trading patterns and cashflow rather than years of filed accounts.

2) Development and heavy refurbishment

Development is rarely neat. Even well-run projects have moving parts.

Banks often struggle with:

- staged builds and drawdowns

- valuation movement during works

- contractor risk and timeline changes

Specialist development finance is designed around those realities, not against them.

More on development finance: howecommercialfinance.co.uk/development-finance/

3) Deals that do not fit a standard bank box

This is the frustrating one. The deal makes sense, but it does not present neatly.

Some examples:

- shorter trading history but strong contracts and a clear plan

- a property that needs work or is unusual in construction or use

- a structure the bank does not like, such as SPVs or multiple parties

- a situation where timing matters more than headline rate

Commercial property is a good example of where this plays out regularly.

For investment properties, most high street banks are reluctant if it’s a first-time investor, if the loan to value is above around 60%, or if there are concerns about the tenants or the let. For owner-occupiers, the issue is often different: the bank wants to see strong profitability to service the debt, and the minimum loan size is frequently too high for smaller business premises. In other words, the banks are more interested in large loans to established companies with consistent financials.

If your deal sits outside those parameters, it doesn’t mean finance isn’t available. It means you need a lender that’s set up for it.

Banks prefer simplicity. Specialist lenders are often more flexible, but the deal still needs to be packaged properly.

4) Sustainable projects with real-world timelines

More businesses are investing in sustainability. Upgrades that reduce energy use, cut waste, or improve resilience.

But lenders still want to see the basics:

- what is being installed

- what it costs

- how it affects the business

- and how the borrowing is repaid

If you are funding a sustainability project, it often sits alongside other needs such as property, cashflow, or expansion, so the structure matters.

More on sustainable project finance: howecommercialfinance.co.uk/sustainable-projects/

Why we can still get these deals funded

Let’s be honest. When people say “the bank said no”, what they usually mean is: “I have asked one lender, and they do not like it.”

Being declined by a bank is more common than most people think. The majority of SMEs won’t satisfy a high street lender’s criteria, not because their business is poor, but because the bar is set very high.

I’d put it this way: being self-employed and going to a high street bank for finance is a bit like going to a Michelin-starred restaurant and ordering cheese on toast. They can probably do it, but it’s not really what they’re there for, and you’re unlikely to get the best result. There are plenty of other options, and some of them will suit you far better.

SMEs shouldn’t let a bank refusal hold their growth back. The alternative lending market exists precisely because the high street doesn’t cover everything, and for many deals it’s actually the better starting point.

The difference with a broker is simple. We are not stuck with one lending box.

The question is not whether finance can help, but how you use it.

My job is to:

- understand the real problem you are trying to solve, such as speed, works, purchase, refinance, or cashflow

- present the deal clearly, including numbers, security position, and exit route

- place it with lenders who actually fund deals like yours

Bridging Finance Solutions

When timing is the biggest risk, bridging can buy you breathing space.

howecommercialfinance.co.uk/bridging-finance/

Development Finance

When the asset is being created or transformed, the funding needs to match the build.

howecommercialfinance.co.uk/development-finance/

Working capital support

Sometimes the deal is fine but cashflow is tight because customers pay late or stock cycles are heavy. That is where invoice finance can help.

howecommercialfinance.co.uk/invoice-finance/

If your bank has refused your loan application, do this next

I would not waste weeks firing off more applications and hoping for a different outcome.

Instead:

- Find out exactly why you were declined. Ask the lender directly. Don’t guess.

- Tighten the case. Forecasts, security position, exit route, and timeline all need to be clear before you approach anyone else.

- Choose the right type of finance for the problem. Speed, structure, working capital, development, and bridging are all different tools. Using the wrong one wastes time.

- Speak to a broker who knows the alternative market. Lender selection and how the case is packaged makes all the difference, especially when time matters.

If you want to talk it through, start here:

howecommercialfinance.co.uk/contact/