Let’s dig into what that actually means…

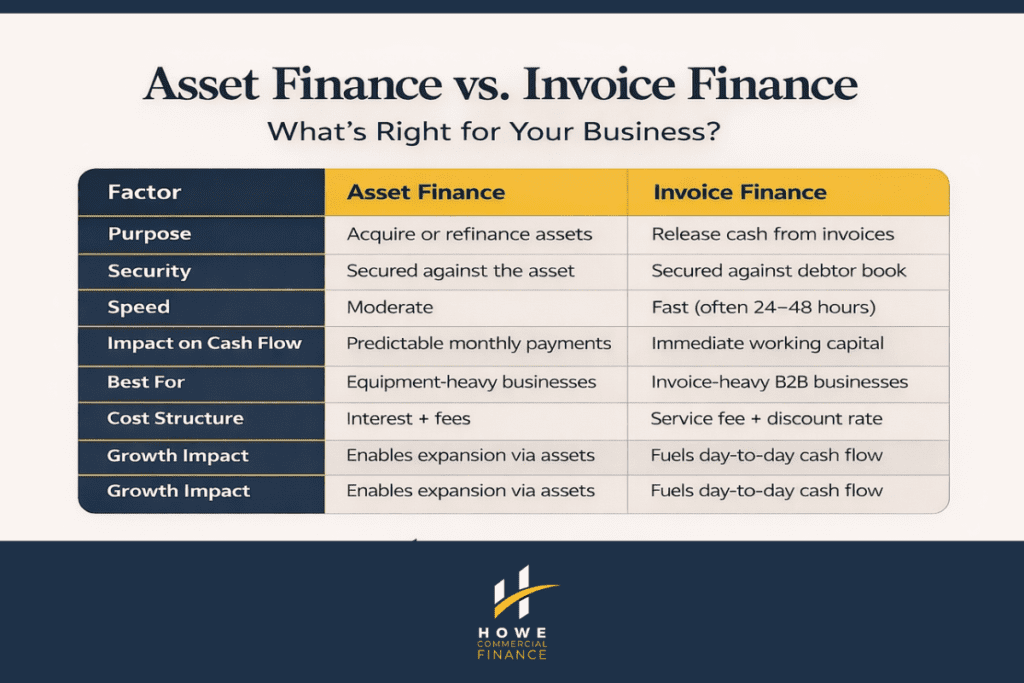

When Asset Finance Makes Sense

If you’re looking to grow and need equipment, machinery, vehicles or tech to get there, asset finance can be a smart move. Rather than paying the full amount upfront, which hits your cashflow hard, you can spread the cost.

There are a few options:

- Hire Purchase – You own the asset at the end of the term.

- Lease – You pay to use the asset for a period, then return or upgrade it.

- Refinance – You use existing assets you already own to release cash.

Example:

Let’s say you run a construction firm and need a new van. With asset finance, you could acquire it now and spread the cost over 3–5 years. Or, if you’ve already got valuable equipment, you could refinance it to free up working capital.

Explore options: Asset Finance Services – Learn More

Asset Finance Services – Learn More

When Invoice Finance Works Better

Got cash tied up in unpaid customer invoices? You’re not alone.

Most B2B companies are working on 30, 60, or even 90-day payment terms. Meanwhile, your own bills don’t wait – staff, suppliers, rent, VAT…

Invoice finance solves that problem by releasing up to 95% of the invoice value straight away, instead of waiting weeks (or months) to get paid.

There are two types:

- Factoring – The lender manages your collections.

- Confidential/Invoice Discounting – You keep control of collections, but invoices are paid to the lender.

Example:

Imagine you’ve just delivered £40,000 worth of work. Instead of waiting 60 days to get paid, you access up to £36,000 the next day via invoice finance. That gives you breathing space to take on new contracts, or just stay current on your commitments.

Find out how it works: Invoice Finance Explained

Many Businesses Use Both – Here’s Why

You don’t have to pick just one. In fact, many of our clients use a combination of both:

Asset Finance to buy the tools and vehicles they need to grow Invoice Finance to cover the working capital gap while waiting for payment

Asset Finance to buy the tools and vehicles they need to grow Invoice Finance to cover the working capital gap while waiting for payment

Together, these tools help you preserve your own cash and plan more confidently.

What Happens If You Do Nothing?

Let’s be blunt. If you don’t invest in better equipment, your competitors will. If you keep waiting on late payments, it’s your business that carries the burden.

And that can mean:

- Missed opportunities

- Inability to fulfil new contracts

- Pressure on wages and tax bills

All of which are avoidable with the right finance structure in place.

The Right Finance at the Right Time – Without the Guesswork

Here’s the thing… there’s no one-size-fits-all answer.

But there is a smarter way to approach business funding.

At Howe Commercial Finance, we help you:

- Understand which option suits your needs

- Access the right lenders (not just the high street)

- Present your business clearly and confidently

- Secure fair, tailored funding that gives you breathing space

No jargon. No generic offers. Just honest advice.

Still Unsure? Let’s Talk.

Whether you’re stuck between options or need to move quickly, we’ll take the time to understand what your business really needs – and help you get it.

Call or message to speak with Paul directly

Call or message to speak with Paul directly Or drop us an enquiry here: Contact Us

Or drop us an enquiry here: Contact Us

Further Reading: